Television

India’s TV distributors are pocketing 80 per cent of your monthly bill and TRAI’s rules are allowing it

A damning survey of 2,037 households by the Esya Centre finds that consumers love television, despise their bills, and have almost no idea why they are paying what they pay

NEW DELHI: Indians are devoted television viewers. They are also furious about what they are being charged for it. A new report by the Esya Centre, a New Delhi technology policy think tank, lays bare a structural dysfunction at the heart of India’s broadcasting sector: a regulatory framework that, intended to protect consumers, has instead handed distribution platform operators an almost unassailable grip on the industry’s money, its channels and its future.

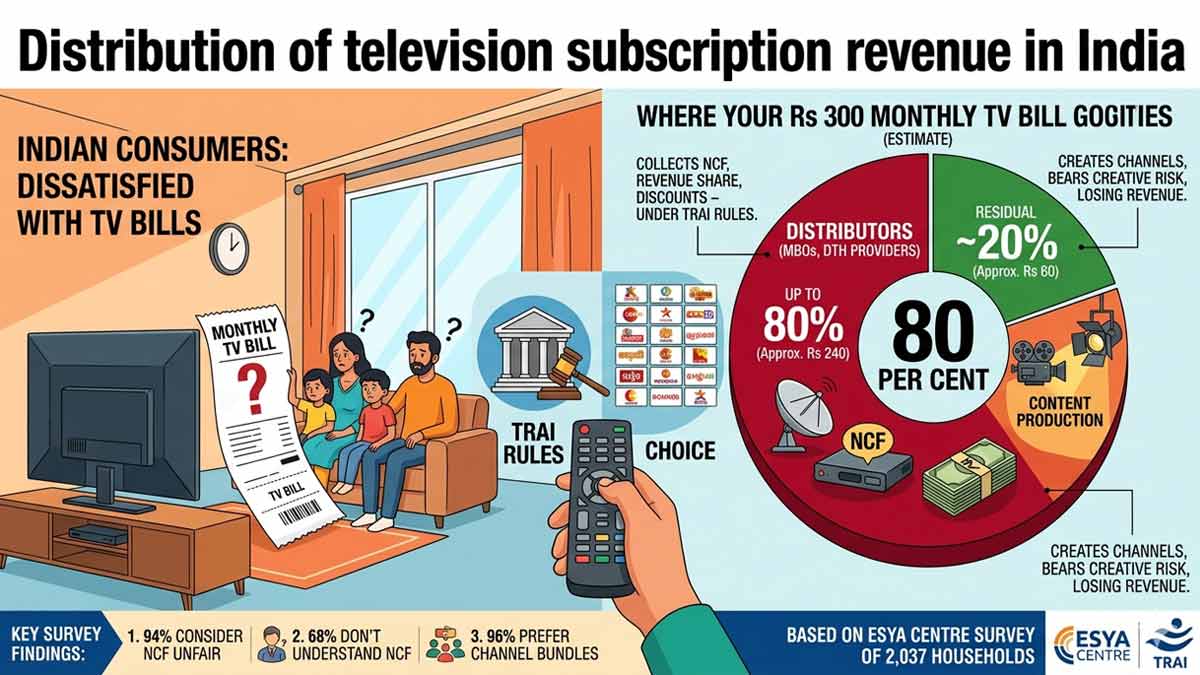

The numbers are stark. Survey data from 2,037 television-subscribing households across 15 cities, collected in December 2025, shows that 70 per cent of respondents are satisfied with the quality of television content. Yet 84.7 per cent report high dissatisfaction with their bills. The problem is not what is on screen. It is what is on the invoice.

The authors, Meghna Bal, director of the Esya Centre, and Shweta Venkatesan, a fellow at the centre, trace the dysfunction to a specific regulatory instrument: the network capacity fee, or NCF. Introduced by the Telecom Regulatory Authority of India in 2017, the NCF is a fixed monthly charge consumers pay simply for access to the television platform, before any pay channels are purchased. Originally set at Rs 130 for up to 100 standard-definition channels, it was deregulated in July 2024 when TRAI introduced forbearance, allowing distribution platform operators to set the fee freely. The results were predictable. Tata Play raised its NCF by Rs 10. Airtel raised its by Rs 15. Competition, the regulator’s stated rationale for deregulation, did not drive the fee down.

The survey’s findings on consumer perceptions of the NCF are withering. Sixty-eight per cent of respondents do not understand what the fee is for or are unaware of it entirely. Ninety-four per cent consider it unfair. Fifty-seven per cent say their monthly bills increased after the introduction of TRAI’s 2017 tariff framework. And 96 per cent say they would be satisfied if the framework were removed. The NCF, the report concludes, is not experienced by consumers as a transparent or justified charge. It functions as what the authors call a platform toll, collected by distributors and not linked in any meaningful way to the cost of actually delivering television signals, which digitisation has made substantially cheaper.

The revenue mathematics that underpin this toll are extraordinary. Under the new tariff order, distributors receive the NCF in full. They are also entitled to retain up to 45 per cent of broadcaster-created bouquet prices as discounts and must receive at least 20 per cent of every pay channel or bouquet’s retail price as a revenue share. The combined effect: on a typical monthly bill of Rs 300, a distribution platform operator can capture up to Rs 240, around 80 per cent of the total, while broadcasters, who actually create and acquire the content consumers are paying for, receive the residual Rs 60. The report is blunt about the absurdity of this arrangement. Broadcasters bear the creative risk. Distributors bear largely fixed transmission and billing costs. The regulatory framework rewards the latter at the expense of the former.

This matters not just for the economics of the present but for the investment incentives of the future. The broadcasting sector is already in visible distress. Approximately 50 television channel licences have been surrendered over the past three years. Dentsu, the media agency, estimates that television’s share of total advertising revenue will fall from 21 per cent to 15 per cent by 2027. Broadcasting disputes filed at the Telecom Disputes Settlement and Appellate Tribunal significantly outnumber telecom disputes year on year, a persistent signal of structural misalignment. The report argues these trends will not reverse unless the regulatory framework is overhauled.

The distributors’ leverage extends well beyond the NCF. The regulatory architecture, the report argues, works as a reinforcing system rather than a collection of isolated rules. Broadcasters are legally required to supply their channels to distributors. Distributors, however, retain discretion over whether to carry a channel, where to place it and how visible it is. This asymmetry is not incidental. It is structural, and TRAI’s rules entrench it.

The carriage fee regime is particularly punishing. Broadcasters must pay carriage fees to distributors if their channels fail to reach 20 per cent of a distributor’s subscriber base in a given market, a threshold raised sharply from the original 5 per cent. For niche, regional and language-specific channels, which serve smaller but intensely loyal audiences, this threshold is a near-impossible bar. The report is scathing about the justifications TRAI has offered for carriage fees. The bandwidth scarcity argument is obsolete in a digitised network. The “unpopular channels” argument betrays a fundamental misunderstanding of how diverse content markets work. A Tamil-speaking household in Uttar Pradesh is not evidence that Tamil-language television is unpopular. It is evidence that India is linguistically complex.

The survey data supports this argument directly. Forty-six per cent of sampled households consume content in non-Hindi languages, including Telugu at 14 per cent, Tamil at 10 per cent, Kannada and Bengali each at 6 per cent, and Marathi at 5 per cent. Nearly half of non-Hindi language viewers report that their preferred channels have become more expensive. Carriage thresholds, the report concludes, penalise dispersed but genuine demand and reduce content diversity by making survival harder for smaller and regional broadcasters.

The bundling rules compound the problem. TRAI prohibits broadcasters from bundling free-to-air channels with pay channels, a restriction justified on grounds of consumer choice and transparency. In practice, the restriction strips broadcasters of their most effective risk management tool. A broadcaster running a portfolio of popular and niche channels cannot use the revenues of the former to subsidise the latter. The survey leaves no doubt about what consumers actually want. Ninety-six per cent prefer a large bundle of channels over a limited selection at the same price. Seventy-eight point two per cent value bundles because they accommodate diverse household preferences at better value for money. Forty point one per cent value them for reducing search costs. Thirty-nine point nine per cent value them for content discovery. Bundling, the report argues, is not a commercial convenience. It is a welfare mechanism. Restricting it harms consumers today and weakens investment incentives for tomorrow.

The report also documents a gap between formal choice and effective choice in channel selection. While 51 per cent of respondents say they select their channel packs personally, 49 per cent rely on distributor-designed plans. More revealingly, 32.9 per cent say that channel unavailability is driven by their distributor’s refusal to carry it. The consumer’s remote control is not as sovereign as it looks. Distributors design the channel menus, the electronic programme guides and the default bundles. What viewers see is shaped before they ever make a choice.

The Esya Centre makes five recommendations. TRAI should introduce immediate forbearance on pricing and packaging restrictions placed on broadcasters. Must-carry obligations should be made unconditional, since digitisation has eliminated the bandwidth constraints that justified conditionality. Carriage fees should be abolished. The NCF should be reduced and distributors should be barred from packaging more than 10 channels in the basic service tier. And fixed-fee deals, under which distributors buy content upfront from broadcasters, should be reinstated, aligning incentives and reducing the torrent of disputes that clogs the tribunals.

The Esya Centre’s survey captures a market in a peculiar kind of trouble: one where 87 per cent of households watch television daily, 97 per cent of those watch daily, and the industry is nonetheless shrinking because the regulatory architecture has arranged for the wrong people to collect the money. Consumers love television. They are paying for it generously. The question the report poses, with considerable empirical force, is why so little of that money ends up with the people who actually make it worth watching.

Sports

Kaacon Sethi retires as CMO of Dainik Bhaskar Group after 12 years

Led brand, content and revenue innovation across media, sports and entertainment.

MUMBAI: After nearly a dozen years of shaping narratives and building brands, Kaacon Sethi is signing off from the marketing playbook at least for now. The long-time chief marketing officer at Dainik Bhaskar Group has stepped down, bringing to a close a 12-year stint that saw her steer the organisation through evolving media and revenue landscapes.

During her tenure, Sethi worked at the intersection of advertising, content and commerce collaborating closely with advertisers to craft client solutions and develop content-led offerings that went beyond traditional formats. Her role increasingly focused on aligning editorial strengths with brand objectives, unlocking new revenue streams in a media ecosystem undergoing rapid transformation.

Her journey at Bhaskar, she noted, was among the most defining phases of her career, one that allowed her to build, experiment and contribute across marketing, branded content and business strategy. From strengthening market presence to driving newer initiatives such as “Urban Bharat”, her work reflected a broader shift in how media organisations approach audience engagement and monetisation.

Sethi also highlighted the collaborative environment within the organisation, describing it as a space where ideas were tested, debated and pursued with conviction, an approach that helped shape several of the group’s marketing and content innovations over the years.

With experience spanning media, entertainment and sports marketing, her exit marks the end of a significant chapter not just for her but also for the organisation’s evolving marketing strategy.

For now, Sethi plans to take a short break before moving on to the next phase of her career. If the past 12 years are any indication, the pause may be brief but the impact is likely to linger longer.